Are Investment Advisors Worth Their Fees?

This Christmas, during a discussion with my family, I could sense hesitancy about the value I add to my clients’ investment portfolios. At times (...2008...), I admit to having doubts regarding the value that we add; but after reading about a 2012 study released by Morningstar, I am comforted by the results.

If you hire an investment advisor only because you expect them to outperform what you could do on your own, or an arbitrary benchmark like the S&P 500, you are forgetting many of the subtle benefits. You shouldn’t hire an independent investment advisor to pick stocks or funds to beat an index, but to help advise you on how best to attain your financial goals, and still sleep at night.

So if out-performance is not what you’re paying us for, then how do we earn our fees?

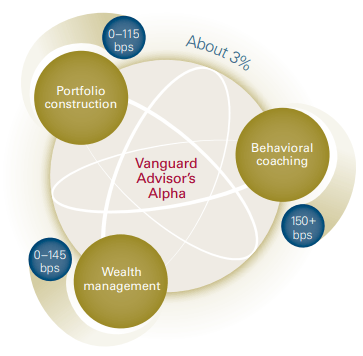

According to the Morningstar study, the ‘Gamma’ (extra income) produced by good investment advice is 1.82% per year—more than covering the average 1% advisory fee. The extra 1.82% of ‘Gamma’—unlike ‘Alpha’, or the ability to beat the market—comes from “following an efficient financial planning strategy.”

There are five parts to an efficient plan:

- Asset Allocation

- Withdrawal Strategy

- Tax efficiency

- Product Allocation (Asset location)

- Liability (goal/needs/timeline)-driven investing

I think two important points were missed in this study: A) Professional advisors take the emotion out of investing, so that the most recent headlines don’t cause reactions and regret. B) We try to bring discipline to your financial life by shining a light on the hard truths about inadequate saving, and encouraging you to be smart with your saving and investing. These two small pieces of the puzzle should not be overlooked.

Conventional wisdom since a study published in the 1990s says that 90% of your investment results are derived from your asset allocation rather than your investment selection. In other words, even a monkey can pick stocks almost as successfully as a human, but what a monkey can’t do is properly expose your portfolio to the yin and yang of a broad set of asset classes. For example: As U.S. stocks are declining, your commodities fund—or another asset class—is rising to offset your losses from U.S. stock.

When it comes to withdrawals, the main points to consider are the rate at which your withdrawals are taxed, and the amount that you can withdraw without risking depletion of your nest egg before your eventual demise. We hope to provide every client with “tax-diversification” in retirement, so that based on your tax bracket, you may choose whether a distribution should come from a tax-free Roth, a taxable IRA, or a non-tax-deferred account. We also counsel clients as to when distributions need to be re-calculated due to changes in interest rates, inflation and expected rates of return.

Tax-efficiency & Asset location are big reasons why an advisor is better equipped to manage a portfolio. Did you know that in most—but not all—cases ETFs are more tax efficient than mutual funds? How about why an HSA may be more tax-efficient than an IRA? Do you prefer 4% dividend income, rental income, or interest income? How about next year? These are issues that we stay on top of, and things that affect how we provide advice on where to save and invest. We have a tax-efficient asset location plan.

Liability-driven investing: If you aren’t going to tap your retirement funds for another ten years, does owning a bond that matures in five years make sense? Maybe. It depends on your risk tolerance, and/or your estimate of upcoming changes in interest rates. Do you plan to pay off your mortgage upon retirement? We invest differently with that kind of knowledge in hand. We need to get to know our clients’ goals, needs and timelines in order to best invest for you.

Did you know that we include a complimentary comprehensive retirement plan for clients with more than $100,000 under advisement? For those of you still accumulating your first six figures, we offer a discounted plan fee of $250. Our plan will alert you if you are under-insured, and remind you to update your estate plan. Most importantly, we’ll let you know if you are on track to retire at age XX; and if you’re not, we’ll suggest small changes that should get you there.

We’re your advisor, not your mutual fund or stock picker. We don’t know how your favorite company’s stock will perform in 2013. But we do know that clients that have gone through the exercise of our comprehensive financial plan have a better understanding of their situation—as do we.

Also, take solace in the fact that Joyce & I eat our own cooking; we invest for ourselves as we do for our clients. Additionally, fee-only registered investment advisors are the most transparent when it comes to fees and performance.

In the spirit of full transparency: we don’t have ‘inside information’ other than what we study. We have no crystal ball. We work with what is available from our clients, the markets, and investment product providers. We live and breathe our fiduciary duty to our clients; we always have and always will act in their best interests. Bring on 2013!