What should I choose - Traditional 401k or Roth 401k?

I’m a big fan of keeping things simple. Unfortunately, our income-tax code has been modified and added onto after seemingly every election cycle. In fact, the current IRS interpretation of the tax code tallies more than 40,000 pages. When it comes to deciding to contribute to a Traditional or Roth 401(k) account, there are many factors to consider – most of which boil down to the amount of income taxes you are projected to pay over your lifetime.

Some of the major factors are:

- Your income tax bracket now

- Your estimated income tax bracket in retirement

- How many years you expect to live (or more simply, your age)

- Your views on guaranteed tax-savings now vs. promised tax-savings later (Do you trust the government to uphold their promises?)

- Your investment return expectations

- Does the state tax you on your income now, and will you retire to a state with or without income tax?

- Your desire to ease the tax burden on your heirs

But first, what is the difference between a Traditional (pre-tax) 401(k), and a Roth 401(k)?

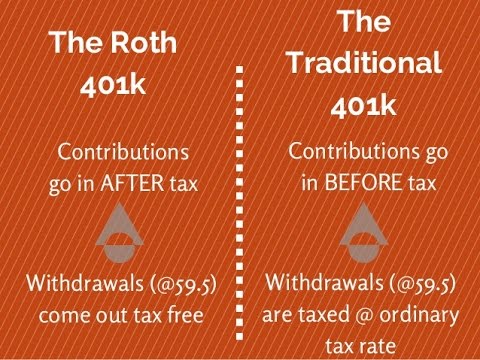

In the Traditional 401(k), your money is deducted from your paycheck before income taxes are calculated. That money is re-directed into your 401(k), having not been taxed (but only avoiding income tax, not Social Security & Medicare taxes). That money can be invested in different types of investments, and as it grows over time, it is tax-sheltered – or not taxed as it grows. This is what we call “tax-deferred” growth. However, when you retire and begin taking distributions from your 401(k) or IRA, those distributions are taxed as ordinary income, which happens to be taxed at the highest rate.

In a Roth 401(k), your contributions come from your net paycheck, after all taxes have been deducted. The money deferred into your Roth 401(k) is allocated to your Roth 401(k) account right before being put in your bank account. But since your contributions were already taxed, the U.S. government promises that if you follow some simple rules, you won’t ever have to pay tax on your Roth 401(k) again. Once you reach age 59.5, you can distribute as much as you want from your Roth 401(k) each year, and none of it will count as taxable income – even the investment gains. This is what we call “tax-free” growth.

Tax-free growth is obviously more favorable than tax-deferred growth. The answer to which type of 401(k) account to use typically comes down to the perceived value of the tax-deduction now in a Traditional 401(k), versus the perceived value of the tax-free growth in a Roth 401(k), accounting for the time value of money. While financial planning software can project the differences in those values, there are many variables – many unknown – that will often cause the projection to be wrong in the real world. What if tax-rates change – and when – and did they increase or decrease? What if I die young? What if I lose money on my investments in my 401k?

We often see tax professionals recommending our clients take as many deductions now as they can, without regard for future tax implications. Unfortunately many tax preparers are only looking in the rear-view mirror, entering information on your tax return from last year. Financial planners like to look out the windshield, and try to determine what the oncoming traffic looks like before helping you make financial decisions.

First, you should determine if it is appropriate for you to participate in your company’s 401(k) at all. If there is no company match or potential profit-share, it’s time to make sure you’ve got other priorities taken care of before participating in a 401(k). Here are my 4 Simple Steps to Financial Success that suggest what your priorities should be, and in what order your disposable income should be allocated:

Step 1: 401k to the match (No match? No 401k contribution yet.)

Step 2: Pay down any debts with interest rates above 6%

Step 3: Health Savings Account (H.S.A.) to the max

Step 4: Roth IRA to the max

You may have noticed that “401(k) to the max” is not listed. Why not? Because it is one of many choices in Step 5.

Did I just mention Step 5 of 4?!?! Yes, because Step 5 is not ‘simple’, it didn’t make the list in our 4 “Simple” Steps to Financial Success. If an employer does not offer a 401(k) match or profit-share, we encourage our clients to skip participating until they’re able to complete through Step 4 each year.

Once you have determined that you should participate in the company 401(k) plan, how do you decide between the Traditional 401k and Roth 401k?

Question #1: Are you in the 12% or lower federal income tax bracket?

- For singles in 2020, that is taxable income less than $40,000, or gross income less than $52,400 (after the $12,400 standard deduction).

- For married couples in 2020, that amounts to taxable income less than $80,000, or gross income less than $105,000.

If you make less than the top figure in the 12% tax bracket, it’s likely a toss-up which 401k account type to contribute to. One additional consideration would be state income taxes, both now and projected in retirement. Or, if you like the idea of a guaranteed tax-deduction now, contribute to the Traditional 401k. If you are young (less than 40), or like the idea of tax-free growth of your investments forever, we think you should choose the Roth 401k. If you pay state income tax now, but plan to move in retirement to a state that levies no income tax, maybe the Traditional 401k is the choice for you.

If your earnings put you in the 22% federal tax bracket or higher, we’d typically suggest that you participate in the Traditional 401(k). A Roth IRA is more flexible than a Roth 401(k),1 so we often suggest Traditional 401(k) to the match in Step 1, and the Roth IRA to the max in Step 4, before filling up more in 401(k) in Step 5. This way, you get the benefits of both the tax-deduction now (401k), and the tax-free growth for later in your Roth IRA –with increased flexibility.

Question #2: Do you think tax rates in the future will be higher or lower than they are now?

Since the passage of the Tax Cuts and Jobs Act in late 2017, tax rates for most Americans are the lowest they’ve ever been. And the individual tax cuts in the Act are set to sunset in 2025, meaning we are all facing a built-in tax-increase in 2026. Only the corporate tax reduction from 35% to 21% remains permanent – for now. And with the government projecting annual budget deficits of $1 trillion or more for the foreseeable future, I can’t imagine tax rates coming down further from here.

Given I expect future tax rates to be higher than current tax rates, I’m more inclined to choose the Roth over the Traditional 401(k) and pay Uncle Sam now at my low rate, in order to avoid paying him later at a high rate. I plan to live the good life in retirement, so don’t envision living off of less income than I am now.

However, once people are retired they become mobile. We have a lot of Oregon clients that retire to Washington, Nevada, or Arizona – which all have either 0% or low-income tax rates. Many Oregon clients’ joint federal and state income tax rates are around 1/3 of their income during their working years, so choosing pre-tax 401(k) contributions is a huge help on their tax bill. If they can avoid the 9% state income tax on 401(k) distributions in retirement, they could plausibly pay a lower tax rate in retirement than during their working years, which would make it more effective to choose the Traditional 401(k).

Question #3: What do I expect my investments to earn in my 401(k)?

If I invest my 401(k) aggressively, I might estimate that I’ll earn an average rate of return of 7.2% in my 401(k) account. If I’m young and aggressive, I should lean toward the Roth 401(k) to take advantage of tax-free compounding of investment results over multiple decades. The Rule of 72 states that at a rate of return of 7.2%, my investment will double every ten years. If my $10,000 at age 20 turns into $160,000 by age 60, that’s $150,000 I won’t ever owe tax on!

If on the other hand I’m nearing retirement, and I prefer to choose the Stable Value Fund in my 401(k) account because I can’t handle volatility, then the Roth 401(k) doesn’t offer much “tax-free growth” given interest rates are near zero. In that case I should lean toward the Traditional 401(k) and take advantage of the tax-deduction now, and simply “defer” any taxes on the small amount of growth the Stable Value Fund might provide.

Question #4: Do I trust the government not change the rules on me?

We hear a lot of clients express their distrust of the IRS and congress – and wouldn’t be surprised if Roth accounts at some point in the future were taxed. Distrust of government is also a reason given for many people who claim their Social Security benefits before the optimal age according to their financial plan.

If you think the rules of the Roth 401(k) game will be changed before you die, that “bird in the hand” of a tax-deduction now is worth more than the ten “birds in the bush” of promised tax-free growth in a Roth account.

Question #5: Am I concerned with leaving taxable assets to my heirs?

For many of our clients, their biggest concern is outliving their assets. In that case, this question is irrelevant. If on the other hand you plan to leave a legacy to your heirs, some up front planning will be much appreciated by your family. Traditional 401(k) accounts inherited by anyone other than a spouse in 2020 and beyond are now fully taxable at their ordinary income tax rate within 10 years (or within 10 years of reaching age 18 if the beneficiary is a minor).

If you’d like to leave your family tax-free assets, getting as much of your retirement funds into Roth accounts should be a priority. We help our clients with Roth conversions in the years between retirement and age 72 (and sometimes earlier, or even into their 90s). One way to avoid having to jump through the calculation hoops of Roth conversions is to contribute directly to your Roth 401(k) – problem solved.

Roth 401(k)s are also not subjected to required distributions at age 72 like a Traditional 401(k). The IRS is anxious to begin collecting tax on tax-deferred retirement accounts, so have created required minimum distribution (RMD) calculations that begin for everyone with a Traditional 401(k) or IRA at age 72. If all of your retirement funds are in a Roth 401(k) or Roth IRA, you choose when to take distributions – and it has nothing to do with income tax rates or penalties on distributions!

After thinking about all of the factors that go into the decision, and asking yourself the five questions, is it any clearer if you should choose a Roth or Traditional 401(k)? If you are still on the fence, the best way to choose – and you can change each year based on new information – is to complete a dynamic, personalized financial plan with a fiduciary financial planner like Sommers Financial Management. We can review and discuss scenarios that will help you determine the best choice for you, based on your priorities, investment strategy, life stage and goals.

- Contributions to Roth IRAs are available any time tax- and penalty-free, whereas your employer controls distributions from your Roth 401(k).